Over the last eight years, the video streaming market has changed for the better… at least for some. In particular, media companies that deliver video to the masses have benefited because they have more choices at lower price points. For some infrastructure companies, the opposite is true – the market hasn’t been good. The massive influx of competition continues to shrink the already thin “industry profit margins”. Streaming as a product is the most commoditized offering in the CDN portfolio.

Before vs Now

Eight years ago, companies of all shapes and sizes who were interested in streaming video, whether it was to a dozen people or the masses, would need to become a platform unto themselves. These companies would pick and choose the individual components, such as the video player, encoder, CDN, etc. to complete the streaming puzzle. There was very little choice and only a handful of expensive platforms. Fast forward to today, and the choices are overwhelming and price points very low.

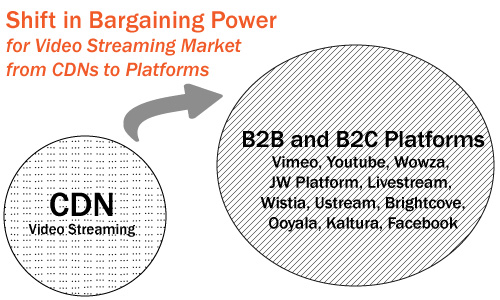

During this period, something very big happened – the competitive landscape changed, and the bargaining power between CDNs and the Platforms shifted. It is now the Video Platform that has the bargaining power when it comes to pricing and leverage. Simply, the Platform companies run the show when it comes to all things streaming. However, the Platform market is also highly commoditized, and the competition keeps everyone in check.

Non-CDN Video Platforms come in many different forms, to those charging nothing, to others charging $20 per month for TBs of monthly video delivery. Some of the more well known ones include Vimeo, Wowza, Brightcove, JW Player, WordPress, Ooyala, Livestream, Ustream, Wistia, Kaltura and Youtube.

The Platforms in the diagram represent some of the players in the market, not all. The business models of these platforms are as diverse as one can get – Vimeo is massive in the B2C space, Brightcove is massive in the B2B market, Kaltura is a builder of Platforms, WordPress Platform is low cost, Youtube is free, and so on.

Video Platform Tiers

- Tier 1: Youtube and Vimeo

- Tier 2: Brightcove, Ooyala, Ustream (IBM), Livestream and WordPress CMS

- Wowza, JW Player and Wistia

As we can see here, there are fewer larger players, and most have economies of scale on their side. As such, they are delivering a bigger chunk of the global streaming market, all the while they consolidate their market power, leveraging Multi-CDNs and DIY CDN, in order to lower their cost structure. In a nutshell, the video streaming business for the CDN is a rough low margin business.